Alternatives strategist for Franklin Templeton Institute, Tony Davidow, shares insights on the role and use of alternative investments in client portfolios with Action! magazine.

Institutions and family offices have historically allocated significant capital to alternative investments, while high-net-worth investors have had limited options due to product availability, investor eligibility and access to certain markets like private equity, private credit and private real estate. Also, the first generation of liquid alternatives provided mixed results.

Consequently, financial advisors have often sought other options to capture alternative-like characteristics.

However, we believe a confluence of events has made alternative investments more appealing for advisors and investors – the markets are demanding broader strategies. Product innovation has made these elusive investments available to a broader group of investors with more flexible features. Now, you can access institutional-quality managers with deep and dedicated resources. We will cover these issues in greater detail in future articles.

What can we learn from institutions?

Legendary investor David Swensen famously stated, “The intelligent acceptance of illiquidity, and a value orientation, constitutes a sensible, conservative approach to portfolio management.” 1

Swensen and many other sophisticated investors recognized the illiquidity premium available by allocating capital to illiquid investments like private equity, private credit and private real estate.

In fact, throughout Swensen’s tenure as the chief investment officer of the Yale Endowment, he often allocated between 70-80% of his portfolio to alternative investments broadly, with illiquidity budgets of up to 50% of their total allocation. The illiquidity bucket is a technique institutions use to identify the amount of capital they are willing to tie up for an extended period (7-10 years).

Of course, endowments are very different from individual investors. Yale has certain built-in advantages, including unique access to private markets, dedicated resources to evaluate opportunities, and long-term horizon. If Yale needs capital, they can reach out to their well-heeled alums and donors for additional capital.

Most high-net-worth investors would be uncomfortable locking up so much capital – but the concept of an illiquidity bucket would certainly apply. While a high-net-worth investor may not have donors to call upon, they often share something with Yale – a long time horizon for some of their goals.

What does the data show?

Academic research has shown the historic persistence of an illiquidity premium2 – the excess return received for tying up capital for an extended time. This makes intuitive sense because you are providing the private fund manager ample time to source opportunities and unlock value. The fund manager isn’t beholden to investors and shareholders, like their public market equivalents, who view results over shorter intervals.

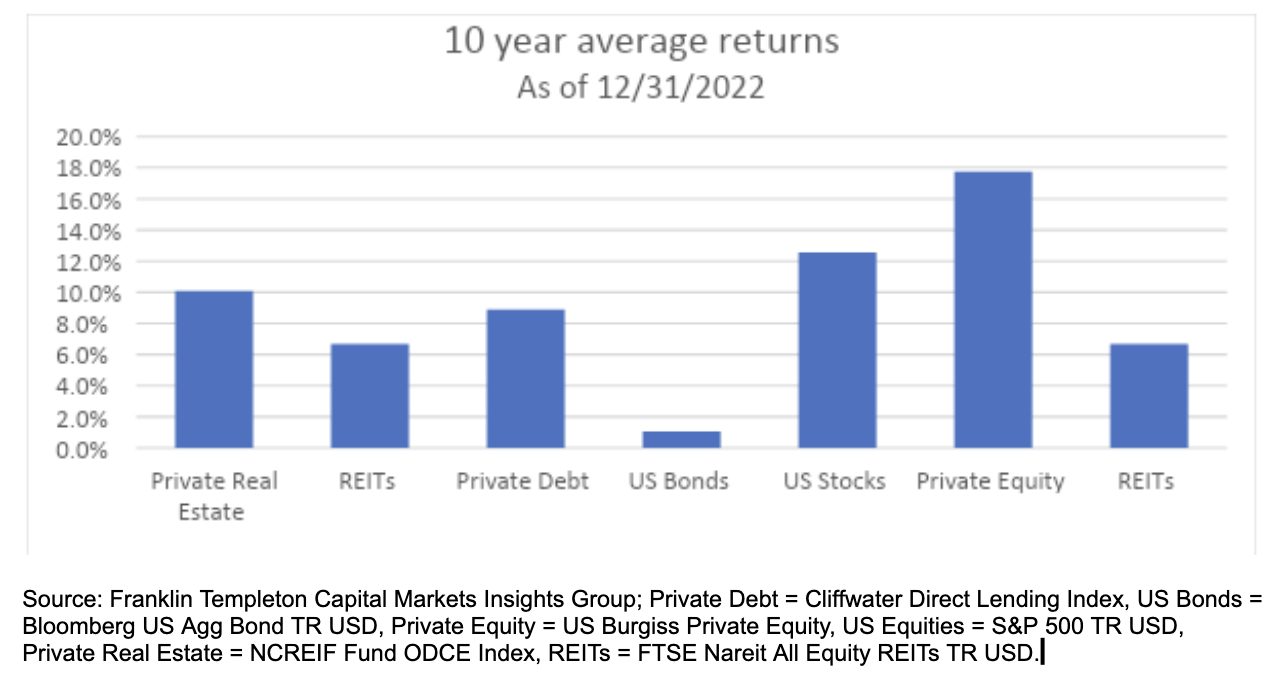

While the magnitude of the illiquidity premium will vary over time, depending upon the market environment and the fund, the data shows that private equity, private credit, and private real estate have historically delivered a substantial illiquidity premium relative to their public market equivalents (see below).

Average 10-year Annual Returns of Private vs. Public Markets

Until recently, high-net-worth (HNW) investors had limited access to these elusive investments due to investor eligibility and high minimums. However, due to product innovation and the willingness of institutional-quality managers to bring products to the wealth management marketplace, HNW investors now have a growing array of options to select from.

How much should advisors allocate to illiquid investments?

The amount of capital allocated to illiquid investments varies by investors and their underlying liquidity profile. Many investors believe they should be 100% liquid – but there is an opportunity cost, especially in today’s market environment. Traditional liquid market investments will likely deliver returns below their historical averages, and advisors may need to consider private markets to help investors achieve their goals.

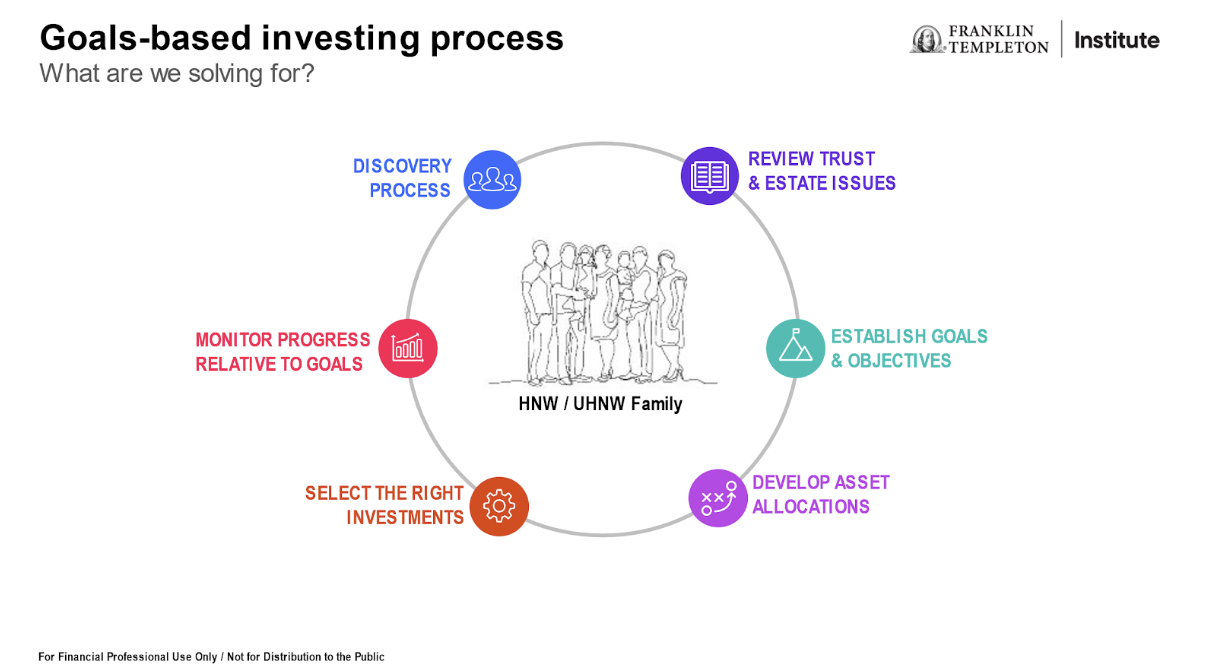

One way of determining the appropriate percentage to allocate to private markets is to develop an illiquidity bucket. Like the Yale example covered earlier, the illiquidity bucket should represent the amount of capital an investor is willing and able to tie up for 7-10 years. It can be determined via the discovery process and advisors should designate these investments as long-term.

As the advisor is determining the family’s needs and requirements, they should inquire about their short and long-term liquidity needs. Do they have significant capital expenditures in the next few years (college funding, purchasing a second home, boat, etc.)? How much of their portfolio needs to be short-term to meet these needs? What portion are they comfortable putting aside for the next 7-10 years?

For many HNW investors, a 10-20% illiquidity bucket may be appropriate given their wealth, income and cash flow needs. Once the advisor has determined the illiquidity bucket, they can define which asset classes are suitable to achieve their goals.

Allocating to private markets

Once the illiquidity bucket has been established for a particular client, you can determine the appropriate allocation to private markets. There are several factors to consider before allocating.

- What are the family’s goals and objectives?

- What is the optimal combination of asset classes (traditional & alternatives)?

- What types of investments provide the highest likelihood of achieving goals?

- Given the investor's wealth and liquidity profile, what is the most appropriate type of fund?

- What is the appropriate amount of capital to allocate per strategy?

As with any investment, advisors must understand and evaluate the many dimensions of a fund before recommending (structure and strategy). Because of the specialized nature of conducting due diligence on private markets, advisors may rely on due diligence conducted by their firm or a third-party provider.

- David F. Swensen, Pioneering Portfolio Management: An Unconventional Approach to Institutional Investment, Fully Revised and Updated

- The Illiquidity Premium and the Market for Private Assets | Portfolio for the Future | CAIA

IMPORTANT LEGAL INFORMATION

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice. This material may not be reproduced, distributed or published without prior written permission from Franklin Templeton.

The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as at publication date and may change without notice. The underlying assumptions and these views are subject to change based on market and other conditions and may differ from other portfolio managers or of the firm as a whole. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market. There is no assurance that any prediction, projection or forecast on the economy, stock market, bond market or the economic trends of the markets will be realized. The value of investments and the income from them can go down as well as up and you may not get back the full amount that you invested. Past performance is not necessarily indicative nor a guarantee of future performance. All investments involve risks, including possible loss of principal.

Any research and analysis contained in this material has been procured by Franklin Templeton for its own purposes and may be acted upon in that connection and, as such, is provided to you incidentally. Data from third party sources may have been used in the preparation of this material and Franklin Templeton ("FT") has not independently verified, validated or audited such data. Although information has been obtained from sources that Franklin Templeton believes to be reliable, no guarantee can be given as to its accuracy and such information may be incomplete or condensed and may be subject to change at any time without notice. The mention of any individual securities should neither constitute nor be construed as a recommendation to purchase, hold or sell any securities, and the information provided regarding such individual securities (if any) is not a sufficient basis upon which to make an investment decision. FT accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments, opinions and analyses in the material is at the sole discretion of the user.

Products, services and information may not be available in all jurisdictions and are offered outside the U.S. by other FT affiliates and/or their distributors as local laws and regulation permits. Please consult your own financial professional or Franklin Templeton institutional contact for further information on availability of products and services in your jurisdiction.