Since 2013, many higher-income US taxpayers have had to pay a 3.8% surtax on net investment income.

Part of the landmark Affordable Care Act signed into law in 2010, this provision was designed to raise revenue to offset other costs including tax credits for consumers purchasing health insurance on the exchanges.

We believe it’s important to understand how this tax applies in order for taxpayers to better manage their tax bill.

Who is subject to the surtax?

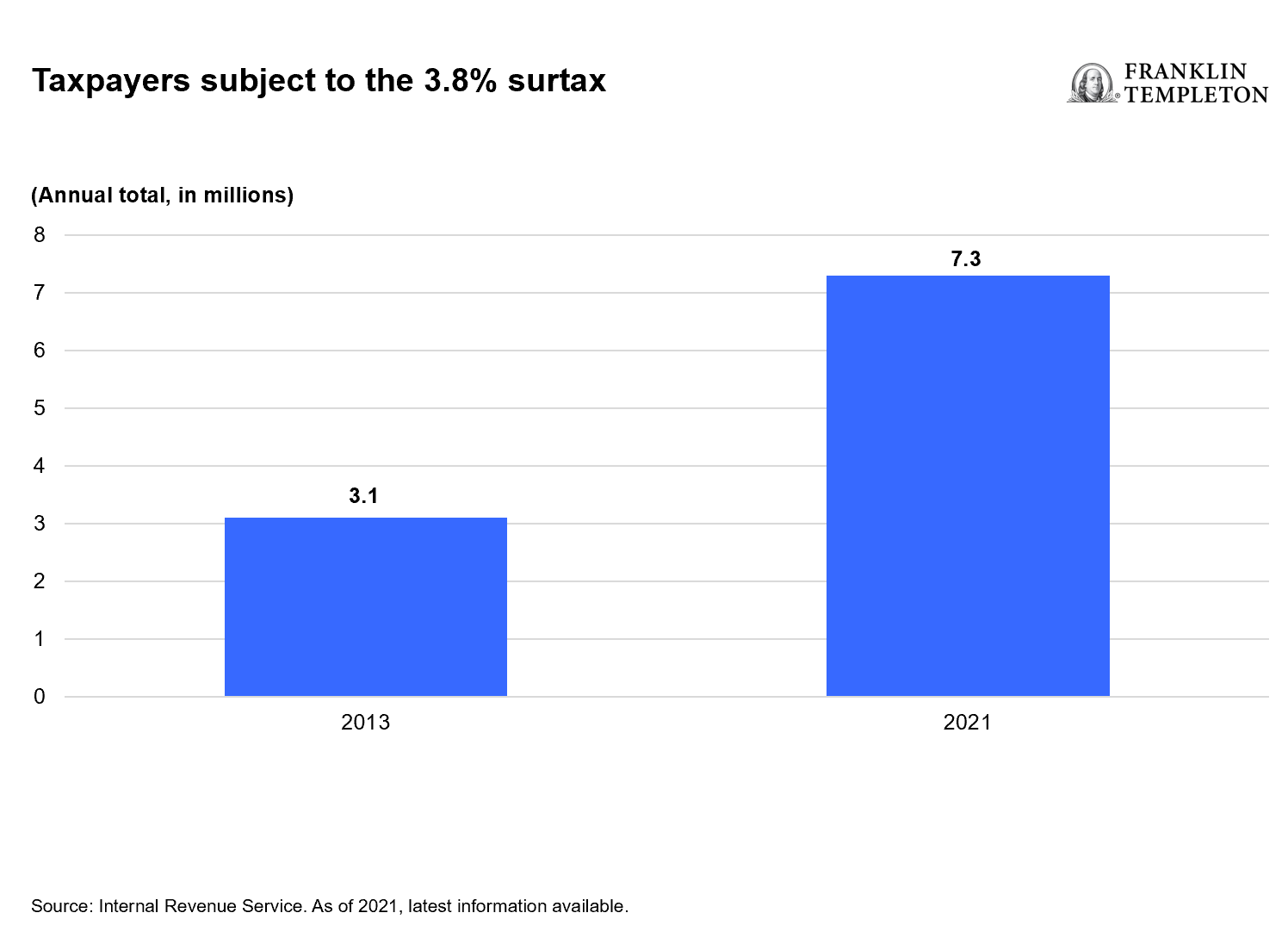

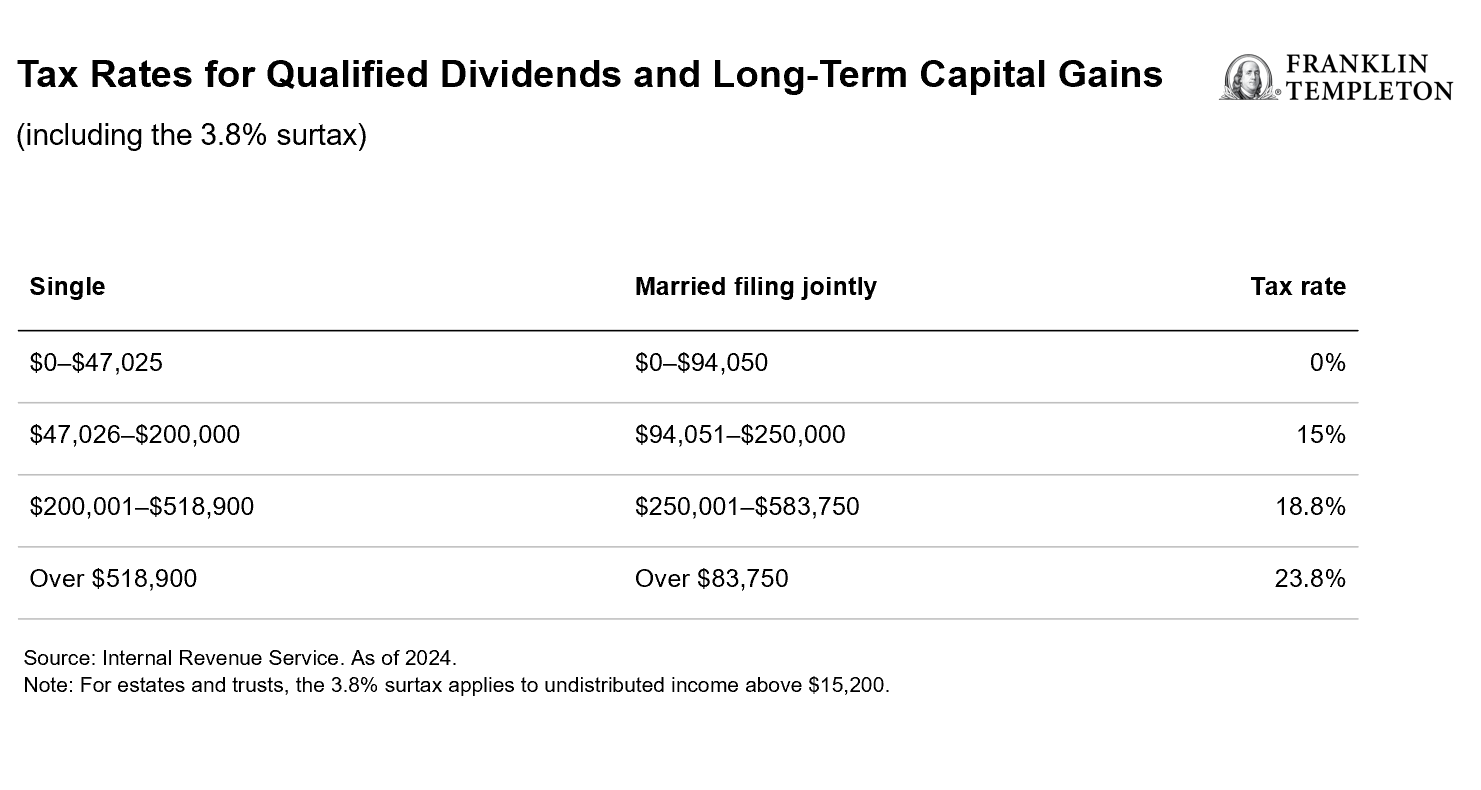

Single taxpayers whose modified adjusted gross income (MAGI) exceeds $200,000 are potentially subject to the surtax. For married couples filing a joint return, the threshold is $250,000. (For married couples filing separately, the MAGI threshold is $125,000). Interestingly, unlike most provisions in the tax code, these thresholds are NOT adjusted for inflation each year which means that more taxpayers are subject to the tax each year. In fact, since its inception, the number of individuals subject to the tax has doubled.

What type of income is subject to the surtax?

The surtax is applied broadly to most non-wage income including interest, dividends, capital gains, royalties and certain rents. Importantly, it does not apply to pension or retirement income, including distributions from retirement accounts and IRAs, or Roth conversions. Other types of income that are not subject to the surtax include:

- Social Security benefits

- Tax-free municipal bond income

- Net unrealized appreciation portion on the distribution of company stock from a qualified retirement plan

It’s important to note that while the 3.8% surtax doesn’t apply to retirement income, an IRA distribution or a Roth IRA conversion may result in additional taxable income and cause a taxpayer to exceed the MAGI thresholds ($200,000 for individuals, $250,000 for married couples filing a joint return), exposing other income sources such as dividends or capital gains to the surtax.

Is business income subject to the surtax?

Certain income generated from pass-through businesses is also subject to the surtax. This would include income sources from passive business activity (rental real estate income, for ex.). Passive activities include trade or business activities in which you don't materially participate. Generally, income derived from a business where the taxpayer is actively participating is not subject to the surtax. You materially participate in an activity if you're involved in the operation of the activity on a regular, continuous, and substantial basis. For more information, see IRS Publication 925, Passive Activity and At-Risk Rules.

Considerations for mitigating the impact of the 3.8% surtax

- Reduce or defer taxable income. Contributions to tax-deferred retirement plans, IRAs, or health savings accounts (HSAs) may enable a taxpayer to avoid exceeding the income thresholds for the surtax. Another way to reduce taxable income is by claiming an itemized deduction, for example charitable contributions. Additionally, there may be ways to defer current income through a deferred compensation arrangement or an installment sale of property, for example.

- Manage income to avoid exceeding the MAGI thresholds. For example, if earning investment income in a taxable account (capital gains, dividends, etc.) and considering a Roth IRA conversion, make sure the amount of the conversion does not result in MAGI exceeding the $200,000 or $250,000 threshold depending on filing status. Exceeding those MAGI thresholds will trigger the additional 3.8% surtax.

- Utilize Qualified Charitable Distributions (QCDs) for annual donations. Requesting a QCD from an IRA can satisfy a required annual distribution. By avoiding income from an RMD, the taxpayer may be able to avoid crossing the income threshold where the 3.8% surtax applies to other income such as interest, capital gains and dividends. See "Donating IRA assets to a charity."

- Consider investing in municipal bonds. Depending on the investor’s circumstances, tax-free income from municipal bonds may help avoid the impact of the surtax. Of course, investors need to carefully weigh the merits from an investment perspective first before considering the tax benefits.

- Reclassify passive business income to active business income if possible. There are steps a business owner may take to avoid income generated from an entity as being defined as passive income. For example, the owner may be able to take an active role to materially participate in the business according to IRS rules. Business owners should consult with a qualified tax professional since these types of IRS requirements can be fairly complex.

IMPORTANT LEGAL INFORMATION

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice. This material may not be reproduced, distributed or published without prior written permission from Franklin Templeton.

The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as at publication date and may change without notice. The underlying assumptions and these views are subject to change based on market and other conditions and may differ from other portfolio managers or of the firm as a whole. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market. There is no assurance that any prediction, projection or forecast on the economy, stock market, bond market or the economic trends of the markets will be realized. The value of investments and the income from them can go down as well as up and you may not get back the full amount that you invested. Past performance is not necessarily indicative nor a guarantee of future performance. All investments involve risks, including possible loss of principal.

Any research and analysis contained in this material has been procured by Franklin Templeton for its own purposes and may be acted upon in that connection and, as such, is provided to you incidentally. Data from third party sources may have been used in the preparation of this material and Franklin Templeton ("FT") has not independently verified, validated or audited such data. Although information has been obtained from sources that Franklin Templeton believes to be reliable, no guarantee can be given as to its accuracy and such information may be incomplete or condensed and may be subject to change at any time without notice. The mention of any individual securities should neither constitute nor be construed as a recommendation to purchase, hold or sell any securities, and the information provided regarding such individual securities (if any) is not a sufficient basis upon which to make an investment decision. FT accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments, opinions and analyses in the material is at the sole discretion of the user.

Products, services and information may not be available in all jurisdictions and are offered outside the U.S. by other FT affiliates and/or their distributors as local laws and regulation permits. Please consult your own financial professional or Franklin Templeton institutional contact for further information on availability of products and services in your jurisdiction.

Issued in the U.S.: Franklin Resources, Inc. and its subsidiaries offer investment management services through multiple investment advisers registered with the SEC. Franklin Distributors, LLC and Putnam Retail Management LP, members FINRA/SIPC, are Franklin Templeton broker/dealers, which provide registered representative services. Franklin Templeton, One Franklin Parkway, San Mateo, California 94403-1906, (800) DIAL BEN/342-5236, franklintempleton.com.