.png)

Beware the ides of March, indeed!

In recent years, capital markets faced unique events during March, each time leading many investors to search for shelter (literally and figuratively). March of 2020 brought COVID-19 lockdowns, March of 2022 brought the Russian invasion of Ukraine into focus, and this year March brought the events of the Silicon Valley Bank (SVB) failure.

Over the last few weeks, I have talked to dozens of our investment managers, clients, researchers and colleagues. This Global Investment Outlook focuses on the most important conversations and takeaways. I hope it helps make a bit of sense out of what just happened – and all the opportunities that lie ahead.

This is not a repeat of the 2008 global financial crisis (GFC). Today’s banking “crisis” is far less severe than 2008, and it’s not systemic. Indeed, the quality of overall bank assets and capital ratios are dramatically better. The central banks are now coordinating globally to offer banks daily access to the capital they need to operate smoothly. SVB failed because of a mismatch between its short-term depositors who were withdrawing assets and its longer-term assets, mostly US Treasuries, that had dropped in value as interest rates increased.

Crisis of confidence

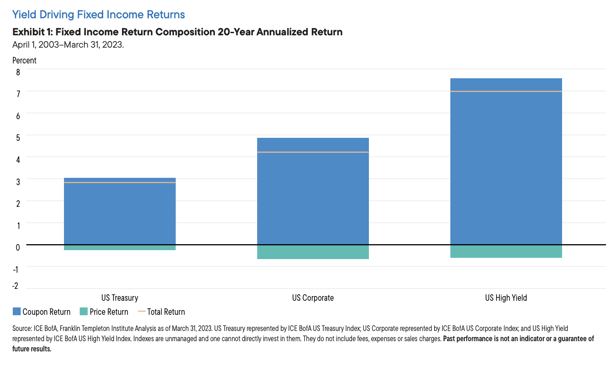

Focus on income

Discerning between those two yield-curve normalization possibilities is a key focus for the Institute throughout 2023. For now, however, our focus within equities is a “barbell,” composed of more exposure to countries, regions and sectors likely to benefit from China’s reopening, complemented by higher-quality, dividend-yielding equity holdings in the United States. Importantly, during periods of elevated inflation, returns from dividends become more significant.

From 2000–2022, for instance, when inflation exceeded 2.5%, the MSCI US High Dividend Index outperformed the MSCI US Index by 11.5%.5 The same is true during episodes of Fed rate hikes, when the MSCI US High Dividend Index generated higher returns than the MSCI US Index 78% of the time.6

Equally, during periods of financial stress, income-focused equity allocations have provided more resilient return profiles. During the 1970s and 1980s, for example, high inflation and interest rates created a challenging environment for stocks, and equity income indexes outperformed broad equity indexes. The same is true when the technology bubble burst in 2001, as equity income indexes, which were less exposed to the technology sector, outperformed the broad market. Finally, during the 2008 financial crisis, equity income indexes also outperformed broad equity indexes as investors sought out more stable and reliable sources of income.

Increase quality through shifting sector and global allocations

Another big equity story for the rest of 2023 is apt to be the attractiveness of non-US stocks, reversing a significant trend lasting more than a decade. One of the reasons is China’s re-emergence from COVID-19 lockdowns, supported by a policy easing – most recently evidenced by a cut in banks’ required reserve ratio.

The other reason is a theme of resilience in Europe, which has held up and adapted better, and faster, than expected to the challenges posed by the Russia-Ukraine war. Those factors offer opportunities for investors. Equity markets outside the United States – in China, the emerging markets complex, and Europe – command lower valuations than the United States. Should growth and earnings prospects improve in those regions as China pivots, then more favorable absolute and relative valuations in non-US equity markets could provide a springboard for performance potential.

Lastly, we continue to underscore other secular trends as opportunities for long-term investors. Dislocations due to high inflation and interest rates have, if anything, created more favorable entry points in sectors such as biotechnology, alternative energy or the digital ecosystem—all areas we believe have excellent long-term growth prospects.

Finding selective opportunities

In sum, the continuing message for 2023 is one of selective opportunities. Differences in growth rates, macro policies and valuations will create differentiated outcomes in the year ahead. We believe investors are likely to be rewarded in higher-quality fixed-income and dividend yield allocations, and on the equity side, looking across the globe—with an eye on emerging markets—makes sense to us. As a result of recent dislocations, areas such as private equity, private credit and commercial real estate also might be viewed with a new lens. Using episodes of market weakness to build positions in the industries of tomorrow is, as always, a prudent strategy for long-term investors.

Sources:

1. Masters, B, Harriet C, and K. Duguid. “Money market funds swell by more than $286bn amid deposit flight,” Financial Times, March 26, 2023.

2. Stone, B. “How You Can Monitor The Severity Of The U.S. Banking Crisis,” Forbes, March 26, 2023.

3. Transcript of Chair Powell’s Press Conference, March 22, 2023.

4. Analysis by Franklin Templeton Institute, SPDJI, US Department of Treasury, Macrobond. Indexes are unmanaged and one cannot directly invest in them. They do not include fees, expenses or sales charges. Past performance is not an indicator or a guarantee of future results.

5. Analysis by Franklin Templeton Institute, MSCI Indices, Macrobond. Notes: Rising interest rate means an increase in US policy rate over the calendar year. Higher inflation means more than 2.5% inflation for the calendar year in the United States. Indexes are unmanaged and one cannot directly invest in them. They do not include fees, expenses or sales charges. Past performance is not an indicator or a guarantee of future results. MSCI makes no warranties and shall have no liability with respect to any MSCI data reproduced herein. No further redistribution or use is permitted. This report is not prepared or endorsed by MSCI.

6. Ibid.